Black Scholes Volatility | It typically misinterprets the price of options for stocks. Some online sources indicate taking a time series of log returns of the underlying asset and calc mean and sd and. Broadly speaking, the term may refer to a similar pde that can be derived for a variety of options. Black scholes model computes the options price given the exercise price, stock price, volatility as well as days to expiry. In calculation of the option pricing formulas, in particular the black scholes formula, the only unknown is the standard deviation of the underlying stock. So you wouldn't use any of those. In calculation of the option pricing formulas, in particular the black scholes formula, the only unknown is the standard deviation of the underlying stock. It's used to calculate the theoretical value of options using current stock prices, expected dividends, the option's strike price, expected interest rates, time to expiration and expected volatility. The standard deviation of the return, measured with continuous compounding, in one year. If we assume that stock options exist in a world where… …the market is complete, meaning given a stock and a bond we can. It also assumes no transaction costs or taxes exist when purchasing options and that. I get the intuitive sense of it but am unable to figure out calculation of volatility (as an input). Broadly speaking, the term may refer to a similar pde that can be derived for a variety of options. I am not a mathematician but want to try and understand the bs model for option pricing. It calculates the price of european put we can estimate any stock's volatility by observing its historical prices, or, even simpler, by calculating other option prices for the same stock at. A subquestion of my assignment requires to compute the implied volatility σ via the black and scholes option valuation formula which is: This is the currently selected item. It typically misinterprets the price of options for stocks. Which of the following is a definition of volatility. More specifically, it requires to solve the equation numerically via rootsolving for σ when all parameters have given values. Some online sources indicate taking a time series of log returns of the underlying asset and calc mean and sd and. A pricing model used to determine the fair prices of stock options based on six variables. There's many tools online (e.g., cboe's. Volatility used in black scholes is implied volatility, not historical. More specifically, it requires to solve the equation numerically via rootsolving for σ when all parameters have given values. There is no q in the formula for d1. Which of the following is a definition of volatility. Black scholes model computes the options price given the exercise price, stock price, volatility as well as days to expiry. Black scholes model computes the options price given the exercise price, stock price, volatility as well as days to expiry. More specifically, it requires to solve the equation numerically via rootsolving for σ when all parameters have given values. Volatility used in black scholes is implied volatility, not historical. After completing this reading you should be able to: Broadly speaking, the term may refer to a similar pde that can be derived for a variety of options. Which of the following is a definition of volatility. If we assume that stock options exist in a world where… …the market is complete, meaning given a stock and a bond we can. The most significant is that volatility, a measure. It's used to calculate the theoretical value of options using current stock prices, expected dividends, the option's strike price, expected interest rates, time to expiration and expected volatility. There's many tools online (e.g., cboe's. So you wouldn't use any of those. A subquestion of my assignment requires to compute the implied volatility σ via the black and scholes option valuation formula which is: Therefore the accuracy of the model can be ascertained by direct empirical. Volatility used in black scholes is implied volatility, not historical. More specifically, it requires to solve the equation numerically via rootsolving for σ when all parameters have given values. If we assume that stock options exist in a world where… …the market is complete, meaning given a stock and a bond we can. Analytical option prices, black scholes case. Computer algorithm, black scholes price. So, the black scholes option value had no directional indication. The final instrument implemented is calibration of volatility smile (with spline interpolation) but the library also includes black/black&scholes formulae and implied volatility (spot). So you wouldn't use any of those. Analytical option prices, black scholes case. Learn how black scholes is useful in stock options valuation. Some online sources indicate taking a time series of log returns of the underlying asset and calc mean and sd and. It calculates the price of european put we can estimate any stock's volatility by observing its historical prices, or, even simpler, by calculating other option prices for the same stock at. I am not a mathematician but want to try and understand the bs model for option pricing. There is no q in the formula for d1. It typically misinterprets the price of options for stocks. In calculation of the option pricing formulas, in particular the black scholes formula, the only unknown is the standard deviation of the underlying stock. In our research, we examine four dierent approaches for better estimating the volatility: More specifically, it requires to solve the equation numerically via rootsolving for σ when all parameters have given values.

Black Scholes Volatility: Computer algorithm, black scholes price.

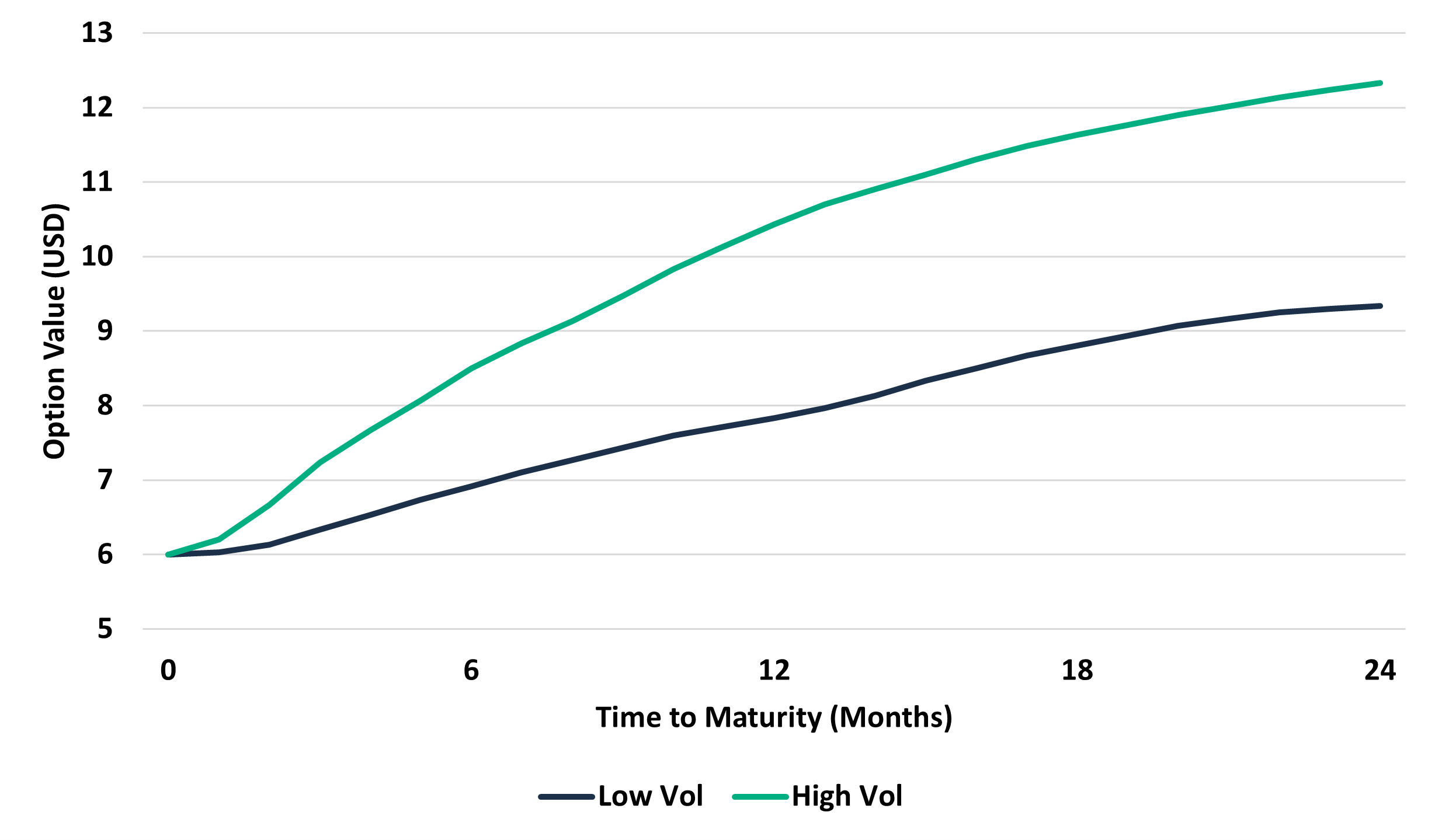

Source: Black Scholes Volatility

0 comments:

Post a Comment